Private Banks and NBFCs vs Public Banks: Who wins?

The Banking and Financial Services Industry (BFSI) is unique. You see, irrespective of which sector/industry a company might be in, they have to interact and do business with at least 1 entity from the BFSI industry – most commonly a bank.

The industry is arguably one the most important of them all and forms the backbone of the country. The BFSI industry is responsible for being the custodian of funds of the public as well as large institutions and it is also responsible for efficiently allocating and lending capital to those pockets of the economy that need it the most.

The banking space comprises Public Sector Banks (PSBs) – that are government-owned, private sector banks and Non-Banking Financial Companies (NBFCs). Let’s look at the industry through a looking glass to identify where opportunities for investors lie.

Overview of NBFCs in India

A non-banking financial company (NBFC) is a monetary institution that performs most of the functions of a bank such as providing loans for various purposes, financial leasing, bill discounting etc. However, unlike banks, NBFCs cannot accept deposits or issue cheques drawn on themselves. Normally, a conventional bank accepts deposits and in turn lends out that money as loans for a slightly higher rate of interest – thereby earning a spread – also called interest margin. However, since NBFCs are not allowed to accept deposits, they raise money from banks and mutual funds, which they, in turn, lend out as loans for a slightly higher rate of interest.

Based on the nature of the business, NBFCs can be classified as – asset finance companies, loan companies, investment companies, infrastructure finance institutions, microfinance institutions, factoring firms, infra debt funds or housing finance companies. Bajaj Finance Ltd, Housing Development Finance Corporation (HDFC), Indiabulls Housing Finance., and LIC Housing Finance are some of the popular listed NBFCs in India.

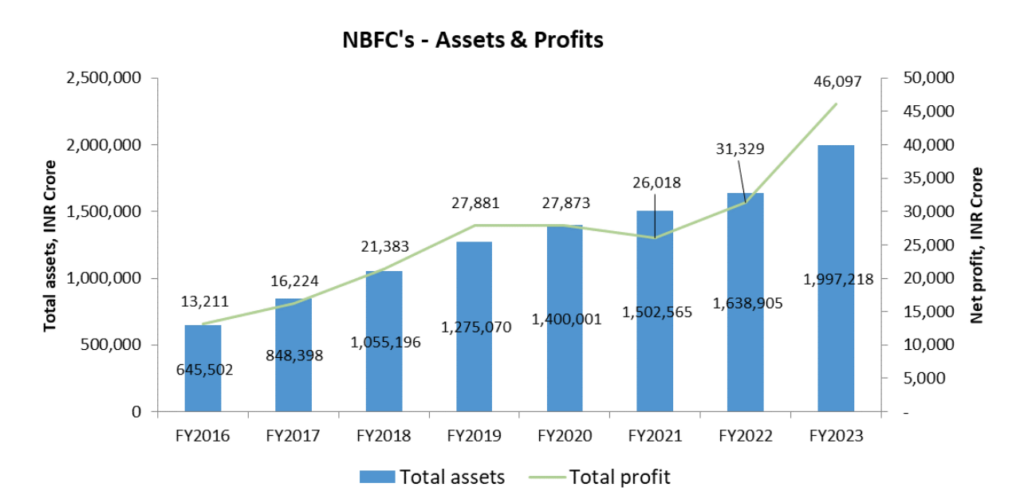

The NBFC sector in India has undergone a significant transformation over the past few years and is today seen as an integral part of the Indian financial system. NBFCs have played a key role in the development of the infrastructure segment. Over the past few years, a significant chunk of debt financing for infrastructure projects has been flowing in from NBFCs. They have also been providing credit to retail customers in underserved and unbanked areas, playing a key part in advancing the Governments programme of financial inclusion.

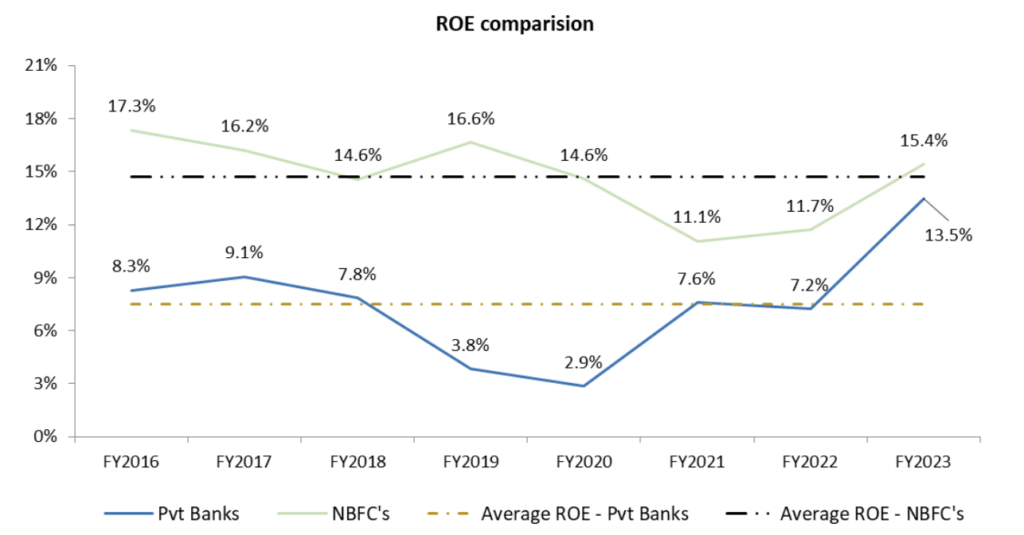

NBFCs have been building their business in areas like Micro, Small and Medium Enterprise (MSME) finance and mortgage products. This is evidenced by increasing assets of NBFCs as a percentage of banking assets. Moreover, very interestingly, NBFCs usually target underbanked segments of the population. This allows them to earn higher profits compared to banks, leading to a higher return on equity.

2018 was the first time when a crisis in the NBFC sector came to light when some of the big names of the sector started defaulting on their repayment obligations. Having said that, the govt. proactively in tackled the crisis in a way that it didn’t blow up to become an economy-wide contagion.

Further in 2020-21, the pandemic was another roadblock for NBFCs as there was a sharp decline in economic activity, which in turn led to a lower demand for credit. In addition, the pandemic also led to an increase in defaults on loans. This was due to a number of factors, including job losses, business closures, and a decline in income. The increase in defaults put further pressure on NBFCs, as they had to set aside more money to cover these losses. Post COVID-19, NBFC performance has significantly improved as economic activity and demand for credit has improved. Other secular trends like low credit penetration in India compared to other economies and low NBFC credit as a percentage of GDP, when compared to other middle and high-income economies, provides a huge opportunity for NBFCs to grow.

Overview of Private Banks in India

Private sector banks in India include local area banks, payment banks, small finance banks and foreign banks. Most of these banks have been at the forefront of adopting technology solutions like the expansion of ATM networks and internet/phone/mobile banking solutions. They have also been hiring direct selling agents to sell credit products. This has allowed private banks to provide better services and amenities to the customer thereby allowing these banks to offer stiff competition to their public sector peers.

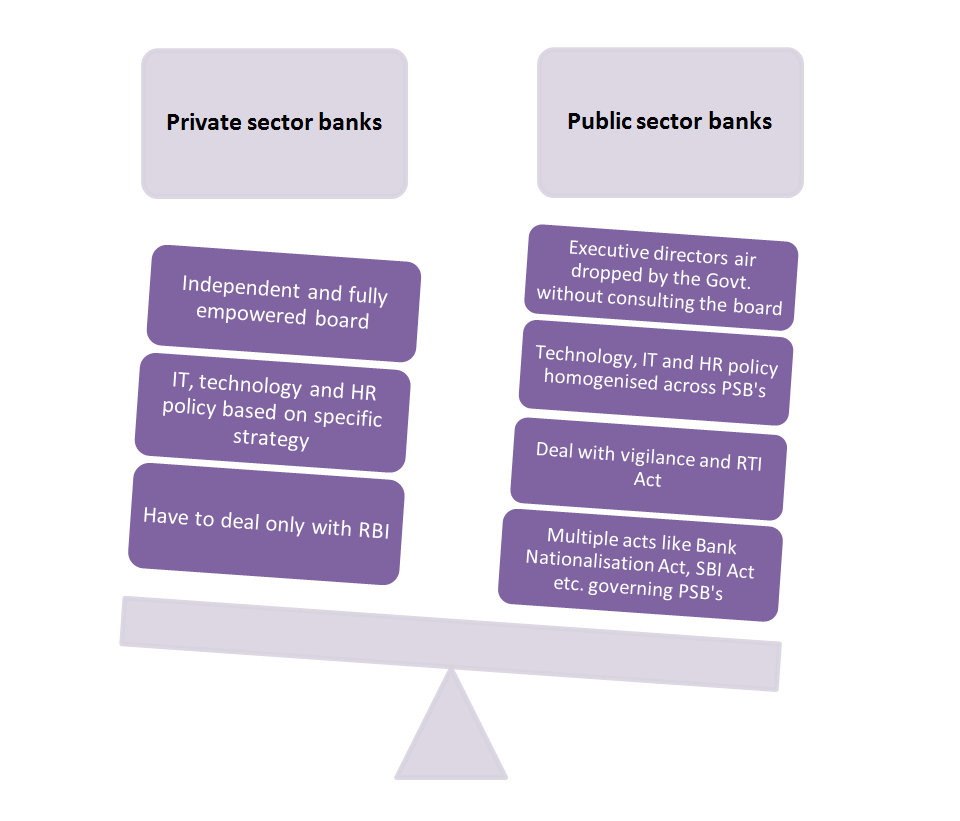

Private banks have certain other advantages compared to public sector banks (PSB).

Compared to 2016, public sector banks have witnessed a drop in their market share – they account for 61% of total banking assets (vs. 75% in 2016) and 58% of total income as of the end of FY18 (vs. 71% in FY16).

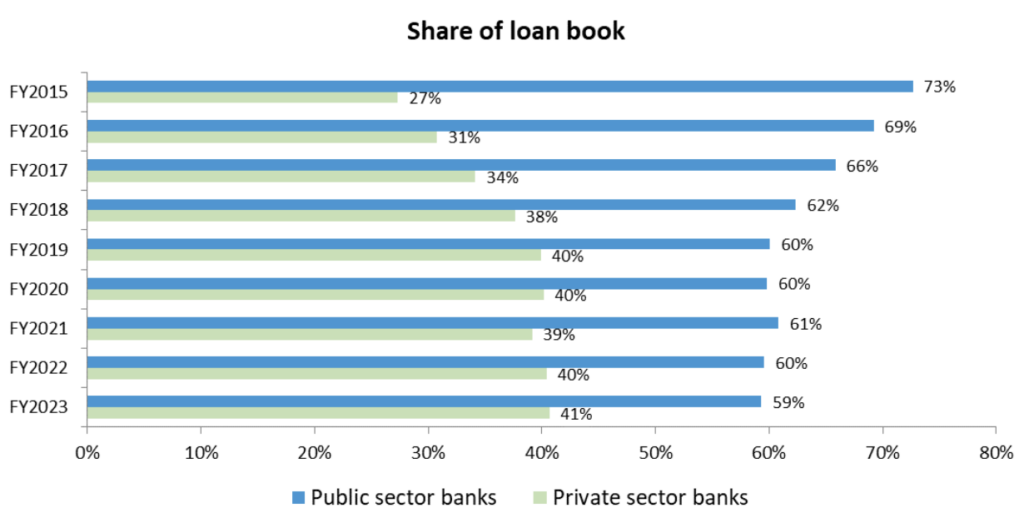

A loan book is a term used to describe the total amount of loans that a bank has issued. Since 2015, private banks have witnessed consistent growth in their loan books, fueled by their superior adoption of technology and stronger retail franchise. In contrast, public sector banks faced challenges related to asset quality issues and capital constraints. However, during FY21, private banks experienced a slight decline in their share of the loan book due to the subdued overall credit demand caused by the COVID-19 pandemic. As the economy recovers and returns to normalcy, private sector banks have begun reclaiming their share in the loan book.

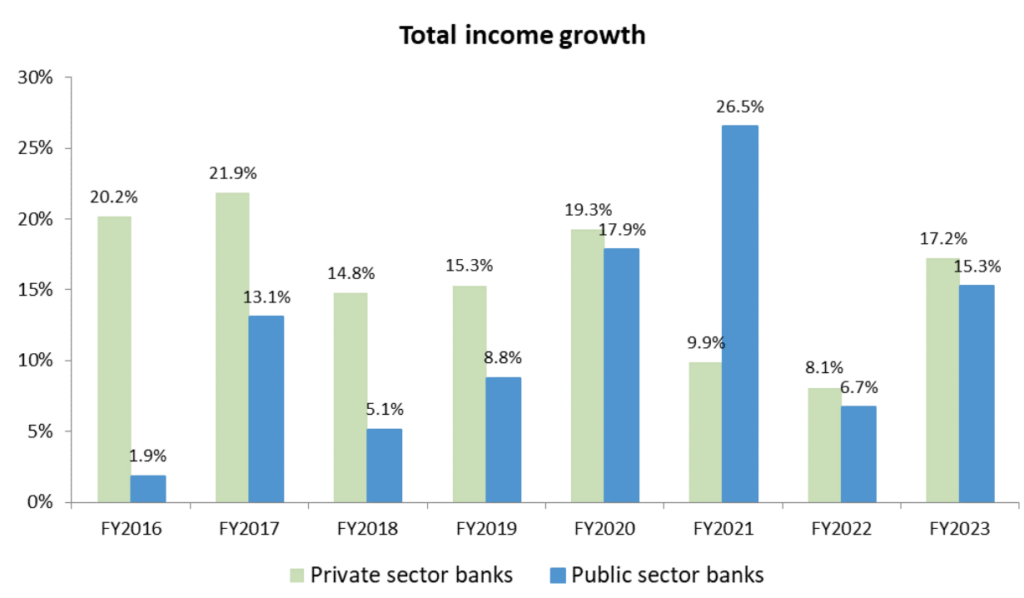

In terms of income growth, private banks have been growing their income at a faster rate as compared to public sector banks.

Non-Performing Assets (NPAs)

Higher inflation, cyclical downtrend and the coronavirus pandemic have led to a drastic drop in demand across various sectors. This has led to losses and companies have not been able to service loans that they had availed from banks. As a result, such loans turned “bad” and banks have had to write them off.

Following the 2008 financial crisis, non-performing assets (NPAs) began to rise among public sector banks (PSBs), peaking in 2018. However, since then, PSBs have made remarkable progress, with the gross NPA ratio declining from 14.6% in March 2018 to 5.53% as of December 2022. In contrast, private sector banks have consistently maintained a significantly lower NPA ratio, ranging between 2-5%.

Additionally, the effect of higher NPAs on return on assets is more prominent in the case of PSBs. The average return on assets of PSBs between 2020 – 2023 was just 0.15% compared to 0.97% for private banks.

Expected revival in economic activity, government support wherever required and relatively normal monsoons are all expected to improve prospects of the banking sector going forward. As the Indian economy grows, the one underlying sector that fuels this growth is certainly going to reap rewards.

Within the banking industry, it’s the private sector banks that are relatively well capitalised, more efficient, and poised and expected to grow faster than PSBs.

Disclaimer: Investment in securities market are subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, membership of BASL (in case of IAs) and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

The content in these posts/articles is for informational and educational purposes only and should not be construed as professional financial advice and nor to be construed as an offer to buy /sell or the solicitation of an offer to buy / sell any security or financial products.

Users must make their own investment decisions based on their specific investment objective and financial position and using such independent advisors as they believe necessary. Disclosures: bit.ly/sc-wc

You may want to read

Building a Core Satellite Investment Portfolio

Building a Core Satellite Investment Portfolio

Getting future-ready with Horizon smallcases 🌅🌿

Getting future-ready with Horizon smallcases 🌅🌿

The Electric Vehicle Revolution and the Role of Batteries

The Electric Vehicle Revolution and the Role of Batteries

Banking Privately

Banking Privately