Inflation Targeting – A Modern Policy Tool

In the previous blog posts, we discussed the nuances of monetary policy and the basics of inflation. If you have not read those posts already, please do so before giving this one a shot – that will help set some context which will help you navigate through this post easily.

The Monetary Policy Objective

Central banks conduct monetary policy to ensure maximum possible employment, stable prices & foreign exchange rates, and maintain a moderate level of interest rate in the long run, allowing for Gross Domestic Product (GDP) growth.

Aspects like employment creation and a stable foreign exchange rate regime can only be indirectly influenced by the central bank.

While a central bank can keep interest rates low to encourage business activity, other aspects like labor laws, property rights, contract enforceability etc. also have significant bearing on growth of businesses.

As for exchange rate management, in the long run, adequate levels of foreign exchange reserves, export competitiveness, and political stability all matter. These aspects cannot be influenced by the central bank effectively.

Central banks, with the authority to change interest rate, are best equipped to deal with the price stability in the economy. This implies avoiding prolonged high inflation or deflation. Price stability is vital for business certainty and supports investment & employment growth.

In short, an economy with a stable price regime is more likely to increase economic welfare. Hence the goal of monetary policy of most central banks is “Price Stability”.

Nominal anchor in Monetary Policy

Once the goal of monetary policy has been established, the central bank then has to decide a specific framework / strategy using which the goal will be chased over the long run. Such a framework will provide not only the structure for decision making regarding monetary policy, but also allows the decisions to be communicated easily to the public.

The monetary policy strategy is based on the choice of a nominal anchor to achieve price stability. A nominal anchor is a single variable that the central bank uses to tie down the price level to achieve price stability. There are 2 kinds of nominal anchors – Quantity based and Price based.

- Quantity Based

- Monetary targeting : This strategy aims to adjust money supply in-line with the underlying GDP growth trend. Money supply in the economy is increased during recessions. On the contrary, the supply of money is slowed down when the economy is booming in order to avoid overheating.

- Price based

- Exchange rate targeting : In this case, the nominal anchor is the nominal exchange rate, for instance the Indian Rupee vs a foreign currency. The central bank deems that it is desirable to maintain the exchange rate of the Indian Rupee vs US Dollar or a basket of foreign currencies at a certain level. It then alters the domestic interest rate as well as intervenes in foreign exchange markets to ensure that the nominal exchange rate level is achieved.

- Inflation targeting : We are finally where we want to be! Here on, we will discuss the nuances of Inflation Targeting.

Inflation Targeting

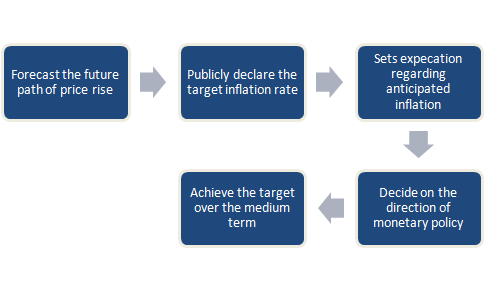

Under this framework, the central bank first forecasts the future path of price rise (basically inflation). It then publicly declares a target price change or inflation rate. The difference between forecast and the target rate helps decide the direction of monetary policy. If the forecast price growth rate is higher than the target rate then the central bank adopts a contractionary monetary policy in order to pull out excess money from circulation. An expansionary policy is adopted in the reverse scenario.

Another important aspect to note is that the central bank does not attempt to hold the target rate at all times. For example, let’s suppose the central bank reviews the inflation rate once every 3 months. It is under no compulsion to adjust the actual inflation rate to the target level for every single 3 month period. The aim is to achieve the target over the medium term – usually over a 2-3 year period. This allows the central bank to react to unanticipated shocks.

For instance, during the Covid-19 situation, most central banks around the world have adopted an expansionary monetary policy with a view to spur economic growth. Hence, inflation will rise in the short term when more money is pumped into the economy. This does not mean that inflation targeting has been abandoned.

New Zealand was the first country to adopt inflation targeting in 1990. By 2000’s, even central banks from emerging economies had started adopting inflation targeting. Currently, more than 70 countries have adopted inflation targeting as the nominal anchor of their monetary policy.

The path to Inflation Targeting in India

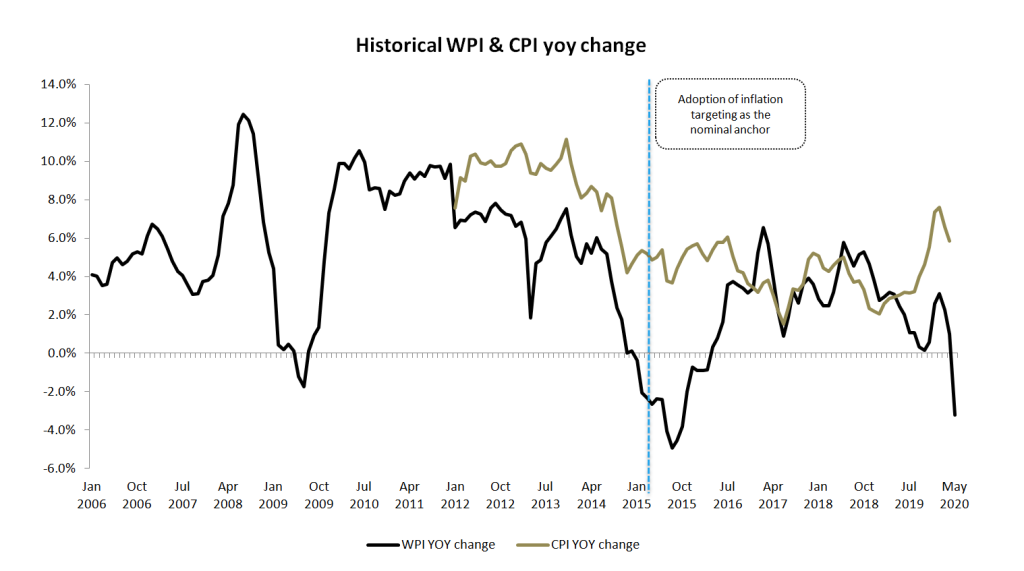

In 1998, India moved away from the monetary targeting regime and adopted a multiple indicator approach as the monetary policy framework. While the Reserve Bank of India (RBI) did not declare an explicit nominal anchor, one of the primary objectives of the new regime was low and stable inflation. RBI would use interest rates to control inflation and the wholesale price index (WPI) was predominantly used to assess inflation.

Though the WPI change was steady at 5-6% during this period, by early 2008 inflation shot up over 10% above the comfort zone of the RBI. This was due to sustained rise in global commodity prices, as well as GDP growth rate in excess of 9% for 3 consecutive years. RBI increased repo rate by a cumulative 300 basis points (3%) to a peak of 9% in order to control inflation. The cash reserve ratio (CRR) was also increased sharply to mop up surplus domestic liquidity.

When the Global Financial Crisis started in 2008, the WPI slumped due to the drop in price of primary commodities. However due to supply side shocks, commodity prices started surging again, pushing up inflation to the 10% range by 2010. Government intervention in the agricultural product and labor market by sharply increasing the minimum support price and introduction of National Rural Employment Guarantee Act also had its effect, resulting in persistently high food inflation. Finally, persistent food and fuel price rise had lowered the credibility of monetary policy, leading to built-in inflation contributing to further inflation persistence.

The absence of a nominal anchor and the subsequent runaway inflation had a disastrous impact on the overall macroeconomic environment. High inflation resulted in erosion of savings, loss of competitiveness and worsening trade deficit.

Based on the recommendations of the Expert Committee to Revise and Strengthen the Monetary Policy Framework Report, the RBI moved away from using WPI as an inflation indicator. The CPI was adopted as the primary inflation indicator and it was endorsed that it would be brought down to hit 8% by Jan 2015 and 6% by Jan 2016. It also agreed to move towards a flexible inflation targeting framework.

In Feb 2015, the Government of India and the RBI signed an agreement formalizing the inflation-targeting framework.

The Finance Act 2016 amended the Reserve Bank of India Act, 1934 to state price stability as the primary objective of the monetary policy. Click To Tweet

A flexible inflation targeting mechanism would be adopted with consumer price inflation (CPI) as the nominal anchor. A monetary policy committee (MPC) would set the policy rate to achieve the inflation target.

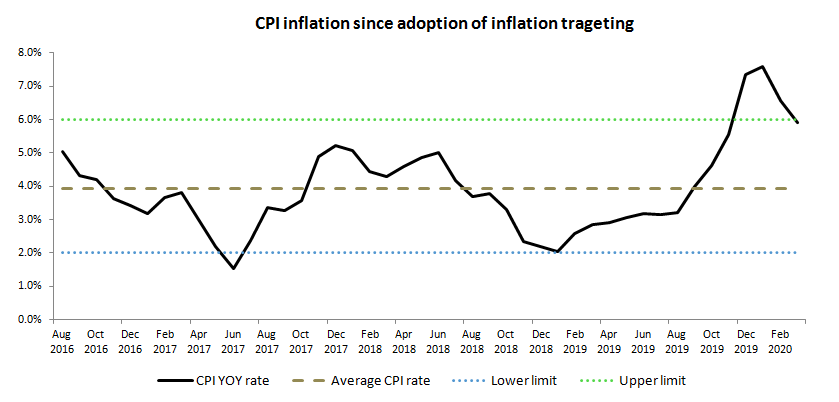

In Aug 2016, a headline inflation target of 4% with 6% and 2% as the upper and lower tolerance levels respectively for the period upto March 31st 2021.

The Aftermath

Since the adoption of CPI inflation targeting, the RBI has successfully ensured that the numbers stay within range. However, the framework is not without its shortfalls.

India’s GDP growth has been trending downwards since June 2018. This calls for an expansionary monetary policy and includes reduction of interest rates. RBI had been cutting the repo rate since Feb 2019 to spur growth. In Dec 2019, the MPC raised its inflation projection to between 4.7 – 5.1% for the second half of 2020, pushed up by transient factors. Immediately the RBI stopped cutting interest rates. This was done to ensure that the “primary goal” of inflation targeting was met and GDP growth issues had to take a backseat.

Several economists are still divided over the idea whether India should be targeting headline or core inflation. The headline inflation includes price changes in food and fuel prices. Prices of these things are susceptible to supply shocks caused due to rainfall, volatile movement in oil price due to geopolitical concerns, etc. Due to such shocks, the prices of these goods record extreme, but temporary, movements within a short period of time. Due to the high weightage of food and fuel in India’s CPI basket, headline inflation can remain quite high for short periods of time. Hence, some economists demand adopting core inflation as the target rate.

Recently, RBI Governor Shaktikanta Das stated that the framework behind monetary policy decision making is being reviewed and discussions will be held with the Government if necessary.

It has not been long since India joined the ranks of countries which have adopted inflation rate targeting as the nominal anchor. The policy is still evolving and we might see more customization that will allow high growth rate while keeping inflation low.

You may want to read

Unlocking India’s Economic Potential: Consumption, Manufacturing, and the Road Ahead (2024 Outlook)

Unlocking India’s Economic Potential: Consumption, Manufacturing, and the Road Ahead (2024 Outlook)

The Power of Capital Expenditure (CapEx): 🏗️ Transforming Nations, Empowering People 💪

The Power of Capital Expenditure (CapEx): 🏗️ Transforming Nations, Empowering People 💪